All Categories

Featured

Table of Contents

Term life insurance is a type of plan that lasts a specific size of time, called the term. You pick the size of the policy term when you first secure your life insurance policy. It could be 5 years, two decades and even more. If you pass away during the pre-selected term (and you've stayed up to date with your costs), your insurance firm will pay out a swelling sum to your chosen beneficiaries.

Choose your term and your amount of cover. You might need to address some inquiries regarding your clinical background. Select the plan that's right for you. Now, all you need to do is pay your costs. As it's level term, you recognize your costs will certainly stay the very same throughout the regard to the policy.

What is the process for getting Level Term Life Insurance Coverage?

(Nevertheless, you do not obtain any type of cash back) 97% of term life insurance policy claims are paid by the insurance business - SourceLife insurance covers most situations of death, however there will be some exemptions in the regards to the policy. Exclusions might consist of: Hereditary or pre-existing conditions that you failed to divulge at the beginning of the policyAlcohol or drug abuseDeath while devoting a crimeAccidents while joining harmful sportsSuicide (some plans exclude fatality by suicide for the first year of the policy) You can include crucial ailment cover to your degree term life insurance policy for an additional cost.Critical illness cover pays a section of your cover quantity if you are identified with a major ailment such as cancer, cardiac arrest or stroke.

After this, the policy finishes and the surviving companion is no longer covered. People usually take out joint policies if they have outstanding financial commitments like a mortgage, or if they have youngsters. Joint policies are typically a lot more affordable than single life insurance policy plans. Other kinds of term life insurance policy plan are:Lowering term life insurance policy - The amount of cover lowers over the length of the policy.

This safeguards the investing in power of your cover amount versus inflationLife cover is a wonderful point to have since it supplies economic security for your dependents if the most awful occurs and you pass away. Your enjoyed ones can likewise utilize your life insurance policy payment to spend for your funeral. Whatever they choose to do, it's great satisfaction for you.

Nonetheless, degree term cover is excellent for meeting day-to-day living expenditures such as house costs. You can additionally use your life insurance policy benefit to cover your interest-only home loan, repayment mortgage, institution costs or any other financial obligations or recurring payments. On the various other hand, there are some drawbacks to level cover, compared to various other kinds of life policy.

How can Level Term Life Insurance For Young Adults protect my family?

The word "level" in the expression "level term insurance coverage" suggests that this kind of insurance coverage has a fixed costs and face amount (survivor benefit) throughout the life of the plan. Basically, when people talk regarding term life insurance policy, they typically describe level term life insurance coverage. For the bulk of individuals, it is the most basic and most budget friendly selection of all life insurance types.

The word "term" right here describes a provided variety of years throughout which the level term life insurance policy remains active. Level term life insurance policy is among one of the most preferred life insurance policy plans that life insurance policy companies provide to their clients as a result of its simplicity and cost. It is additionally very easy to compare degree term life insurance policy quotes and obtain the best premiums.

The device is as complies with: To start with, pick a plan, death advantage amount and plan period (or term length). Pick to pay on either a month-to-month or annual basis. If your premature demise takes place within the life of the plan, your life insurer will pay a round figure of survivor benefit to your predetermined beneficiaries.

How do I choose the right Level Premium Term Life Insurance?

Your level term life insurance policy policy expires when you come to the end of your policy's term. Now, you have the adhering to options: Choice A: Stay without insurance. This option matches you when you can guarantee by yourself and when you have no financial debts or dependents. Option B: Buy a brand-new level term life insurance coverage plan.

FOR FINANCIAL PROFESSIONALS We have actually made to give you with the very best online experience. Your present internet browser could restrict that experience. You may be utilizing an old web browser that's unsupported, or settings within your browser that are not suitable with our site. Please conserve yourself some aggravation, and update your web browser in order to view our website.

What is the process for getting Affordable Level Term Life Insurance?

Currently using an upgraded web browser and still having difficulty? Your present browser: Discovering ...

If the policy expires before your death or fatality live beyond the past term, there is no payout. You might be able to restore a term policy at expiry, however the costs will be recalculated based on your age at the time of revival.

Whole Life Insurance Policy Fees 30 $282 $247 40 $382 $352 50 $571 $498 60 $887 $782 Resource: Quotacy. Quotes are for a $500,000 permanent life insurance coverage plan, for guys and ladies in superb wellness.

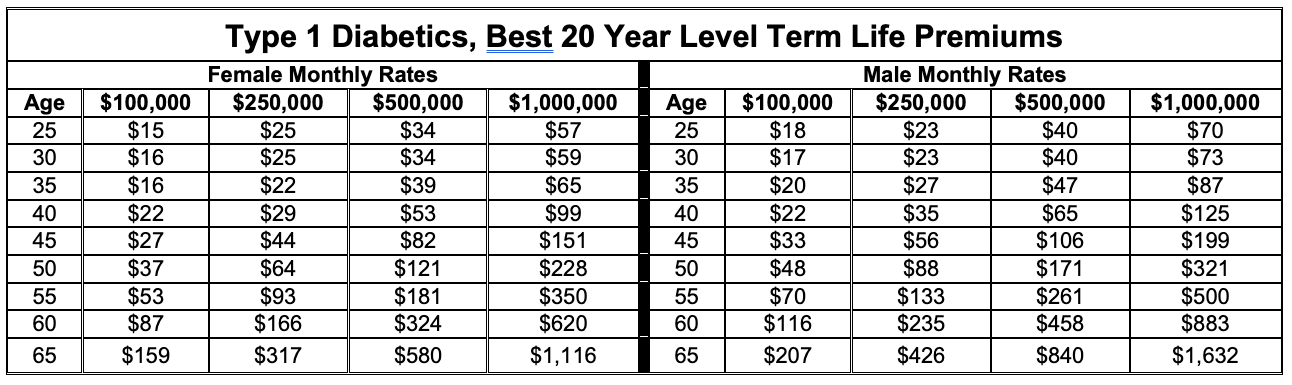

Best Level Term Life Insurance

That decreases the general risk to the insurance firm contrasted to a long-term life policy. The decreased risk is one element that allows insurance providers to bill lower costs. Passion rates, the financials of the insurance provider, and state regulations can also affect costs. Generally, firms usually supply better prices at the "breakpoint" insurance coverage degrees of $100,000, $250,000, $500,000, and $1,000,000.

Examine our recommendations for the ideal term life insurance policies when you prepare to buy. Thirty-year-old George intends to protect his family members in the not likely occasion of his sudden death. He purchases a 10-year, $500,000 term life insurance coverage plan with a premium of $50 each month. If George dies within the 10-year term, the policy will certainly pay George's beneficiary $500,000.

If he lives and restores the plan after one decade, the premiums will be higher than his first policy since they will be based upon his current age of 40 instead of 30. Level term life insurance. If George is diagnosed with an incurable health problem throughout the initial plan term, he probably will not be qualified to restore the plan when it ends

There are several sorts of term life insurance policy. The most effective choice will depend upon your specific conditions. Typically, a lot of companies provide terms ranging from 10 to three decades, although a couple of offer 35- and 40-year terms. Level-premium insurance has a set monthly settlement for the life of the policy. Most term life insurance policy has a level premium, and it's the kind we've been referring to in the majority of this post.

What should I look for in a Level Term Life Insurance Vs Whole Life plan?

Therefore, the costs can become much too pricey as the insurance policy holder ages. They may be a great option for somebody that requires temporary insurance. These plans have a death advantage that declines each year according to a predetermined routine. The policyholder pays a repaired, degree costs for the duration of the plan.

{kind=link}

Latest Posts

What Is Final Expense Insurance Policy

Life Insurance Burial

Instant Insurance Life Quote Whole